Should you decide Play with Good HELOC To fund University against. Student education loans

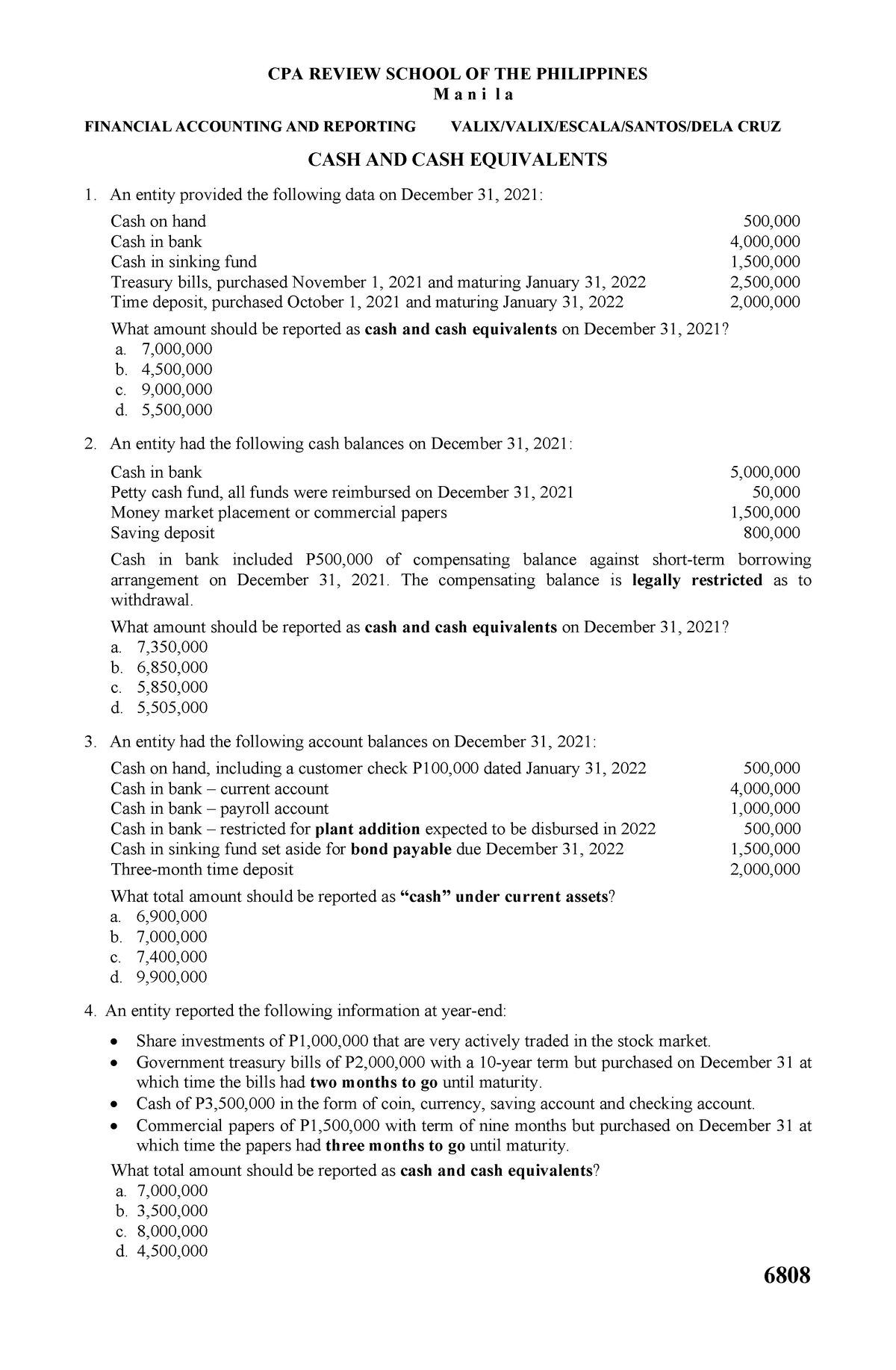

You will find tens and thousands of borrowing products and attributes online, and we believe in assisting you to discover that is best for your, how it functions, and can it really help you achieve your financial requirements. We have been proud of our stuff and you will guidance, and the pointers we offer is objective, separate, and 100 % free.

But we have to return to spend we and keep this web site powering! The partners make up united states. TheCollegeInvestor enjoys a marketing connection with some otherwise most of the even offers provided in this post, that could impression just how, where, and also in what order products and services may appear. The institution Trader doesn’t come with the organizations or offers readily available in the marketplace. And our very own couples will never spend me to verify advantageous evaluations (if not purchase a peek at what they are offering to begin with).

To find out more and you will an entire variety of our adverts people, delight check out all of our full Advertising Disclosure. TheCollegeInvestor strives to store the recommendations specific or over thus far. The information inside our reviews could well be distinct from everything see when going to a lender, provider otherwise a certain product’s website. Every services and products was displayed instead of warranty.

Regarding buying college or university, specific mothers select alternatives such using a HELOC otherwise domestic guarantee mortgage instead of student education loans.

The residence’s collateral may be used not merely to own home improvements however for investing in college or university, or even paying dated student education loans.

In the event that you Have fun with A HELOC To cover College versus. Figuratively speaking

In terms of utilizing your home’s equity, Helen Huang, Senior Movie director from Equipment Deals to own SoFi’s financial items, states there are many masters, Collateral are a hack for enhancing your budget. Use it to repay higher attract credit cards or scholar financial obligation, or to create higher-value improvements to your house-such renovations a cooking area. Banking institutions would like to know you can use the fresh equity sensibly.

To make use of the residence’s collateral, their bank otherwise mortgage lender brings a HELOC otherwise household collateral line of credit. You could capture pulls about line-up with the limitation. Due to the fact range is made, you might remain attracting inside it without the need to fill out a credit card applicatoin whenever.

Rick Huard, an effective TD Financial senior vice president away from individual items, cards, A good HELOC is normally a beneficial 20- otherwise 29-year label.

A lot of things might change-over that time. This enables the customer – without the need to save money money getting closing costs or costs otherwise going through a software process – to carry on to meet up their borrowing from the bank requires across the life time of the experience of us.

On this page, we’ll evaluate using a great HELOC to expend off college loans, along with a few monetary a few.

What’s An excellent HELOC Otherwise Family Collateral Loan?

Good HELOC was property Equity Personal line of credit. This might be financing which you sign up for up against the value of your property, and you may make use of it in the mark period. Your generally shell out desire-only into the draw period, and then you complete repay the loan into the fees months.

A property Security Mortgage is like a HELOC, but there’s zero mark several months. You just pull out one to lump sum payment of cash up against the domestic security.

What does it seem like in practice? If you very own a home worth $800,000, and also home financing out-of $eight hundred,000, you may have $eight hundred,000 off «home equity». These financing allows https://paydayloansconnecticut.com/riverside/ you to make use of that money – always to 75% or 80% of your home’s value. In this circumstance, an 80% HELOC otherwise House Equity Financing setting you could use $240,000.

Deja una respuesta