Keep in touch with a qualified lender about your solutions

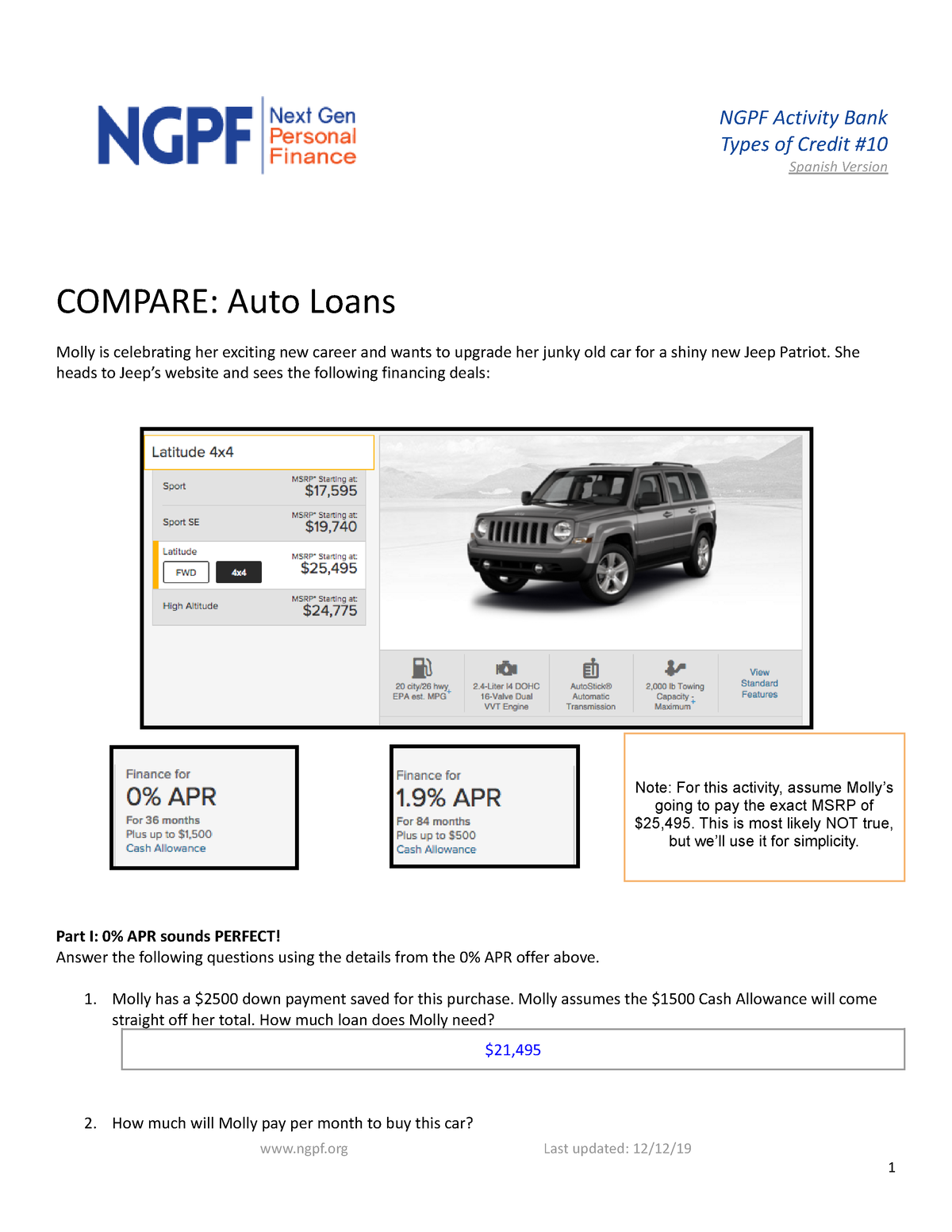

Because the you come from the home buying techniques in advance of, you could potentially become quite safe since you relocate to purchase your next domestic. But not, you might not look out for a few of the previous financial code transform for instance the you to definitely out-of down costs. In order to better learn off costs and some of your this new Canadian financial regulations, we are going to defense it on this page to assist shed people hiccups’ that will allow burdensome for you to get their second family.

As of , you should have at the least 5% of cost of the house once the a downpayment. Whether your house will set you back more than $five hundred,000, you may need 5% from $five-hundred,000 ($twenty-five,000) along with ten% of the remaining matter. Such as, if you wished to get a good $600,000 household, you’d need at the very least $thirty-five,000 once the an advance payment. There is always a choice of paying over the minimum.

not, when buying the next home, lenders essentially require more substantial deposit to the track from 20% or higher. This is due to new guarantee you’ve got currently establish because the a citizen.

Private Financial Insurance policies

Whether your down payment is below 20% of your own price, you will have to buy individual financial insurance (PMI) too. The new Canadian Mortgage and Casing Corporation (CMHC) is the one prominent vendor of such insurance rates. New premium you’ll shell out constantly range from .5 so you can 2.75%. Brand new percentage is then placed into your own monthly financial, a bit broadening those individuals payments.

As you probably remember off purchasing your first household, a larger down payment form down monthly installments. While you are probably a lot more certain on which need for the a home the following go out up to, its worth seated which have a home loan calculator to crunch some wide variety.

Plus, it can be practical to speak with your own builder about precisely how various other framework selection can affect the full price of our home and your mortgage repayment.

For instance, opting for an incomplete basement you will lessen the price of your new domestic adequate that you might pay for 20% down. If a completed basements and additionally a larger down payment are important to your, then you will definitely an inferior house or apartment with a done basement suffice their needs equally well if you’re costing reduced?

A separate method in which the home loan can work for you is to use it to greatly help pay for additional features. For-instance, do you wish to build a fence however, want to spread the price across the lifetime of your home loan? Therefore, up coming including a surroundings otherwise barrier package throughout the get commonly improve your monthly obligations, nonetheless it will also help your prevent investing in it all initial. This way they stops out-of their lawn in the exact same time as your new house is prepared.

Wanting The Down payment

A down-payment you will definitely come from private discounts or perhaps lent from the RRSP. But not, many people just who currently own residential property and would like to transfer to a separate you to definitely utilize the guarantee off their old house just like the a down payment for another you to definitely.

This new equity ‘s the amount of cash you’ve got left when you promote your current family, repay people count which is leftover with the newest mortgage, and shell out people judge fees on the product sales. If you have been residing in your household to possess 10+ decades, it’s possible to have a lot of collateral that you’ll be able to use for your down payment.

But not, if you’ve simply already been living there a couple of years California loans, the majority of your monthly premiums were going on focus, as well as your guarantee may only be adequate to purchase will cost you regarding selling.

Timing Your new Family Purchase

When you wish to sell their old where you can find create a brand new one, you should get a hold of equilibrium inside the timing the fresh new changeover. You’re going to have to promote your household basic discover access to that far-required collateral to possess a down-payment, however also need this new home to be ready for move-when you look at the. That is tough to to-do.

One good way to navigate such oceans is to apply certainly one of all of our popular lenders. As they are familiar with the procedure, they can help you negotiate the acquisition. As an example, you will be able to bring a house guarantee mortgage in order to fool around with because the a down payment, next pay that it away from when you offer your residence.

This new deposit plays a huge role throughout the cost from the new home, and it’s wise to bundle appropriately. Since you work at the builder to develop where you can find your own ambitions, think of just how your options often affect the payment. Set out as much currency that one can to settle brand new most secure updates.

Deja una respuesta