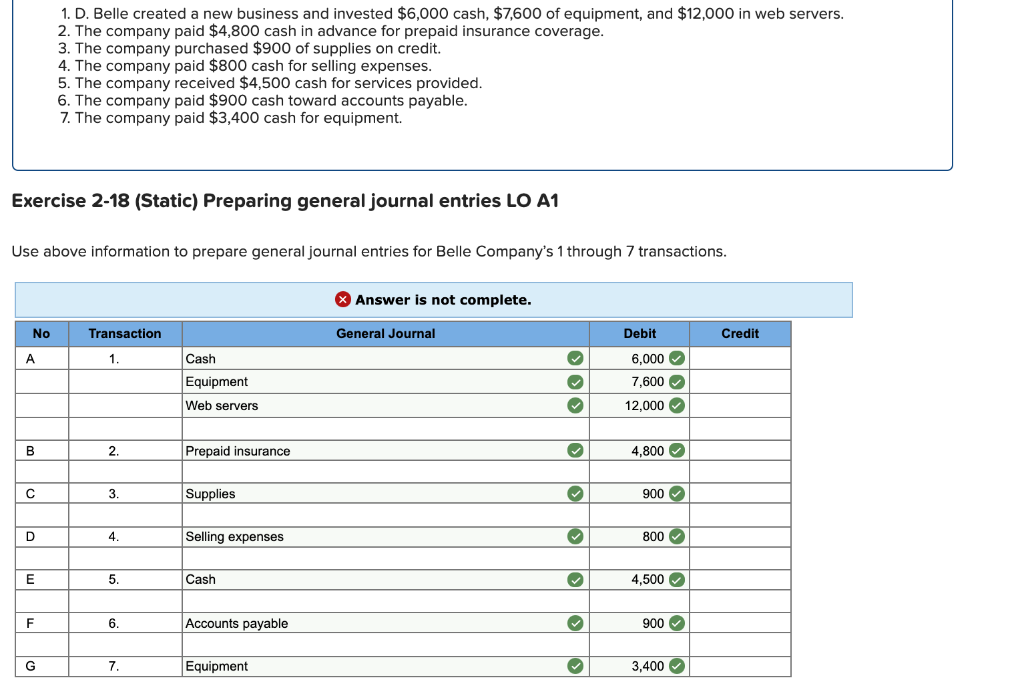

Simply how much Can you Obtain or any other Individual Financial Issues

Brand new huge difference, terms and conditions, and you can reasoning about individual home loan lending would be complicated to own users and other world people. Let’s produce indicated on proper guidelines.

How much Do you really Use?

.jpg)

How much money a debtor have access to depends generally towards just like the-is value of the home to be financed, whether a preexisting property or one that you are going to pick. Venue, position, and property variety of are extremely important.

Loan-to-Worthy of (LTV) is a percentage of your financing to your worth of brand new assets. Particularly, a beneficial 65% LTV mortgage function the financial institution usually advance around 65% of appraised worth of the house, and also the borrower would need to provide the most other thirty-five%. More guarantee otherwise skin-in-the-game you really have, the greater the rate and you can terms would-be. Available LTVs range between bank in order to financial and from problem to problem, however, basically 80% will be the restrict you may expect to possess a prime metropolitan property, however, probably be 65%.

Focusing on how loan providers assess and you may would risk inside the that loan deal is crucial. The primary matter for lender ‘s the possibility your debtor might not pay off the borrowed funds on time or after all, requiring suit. The home loan company, whether or not personal or a conventional lender, need to take into account the after the:

In the event of non-commission, how quickly normally the house or property feel seized, exactly how swiftly is-it ended up selling, and will the financial institution recover their money?

Generally, the fresh court recourse to possess non-fee was foreclosures and you may a required marketing. While the purchases are closed, the brand new continues are marketed on adopting the acquisition: first, the courtroom charge is paid, accompanied by the latest foreclosure lawyer, then your Real estate agent, and finally the loan bank(s). Any kept loans is returned to the newest borrower. By the capping the utmost financing or Financing-to-Well worth (LTV) commission, loan providers try to verify there is certainly sufficient currency left to recoup their dominating and you will interest. Highest LTVs are around for more suitable characteristics which can be easier and you can less to market, whenever you are lower LTVs are typical to possess features which can be more complicated to offer on time. Highest LTVs otherwise quicker money pose greater dangers having loan providers, as there may not be adequate fund remaining to recoup their loan once data recovery expenditures in case of standard.

How many Financial are permitted toward a home?

You’ll have one or more home loan to the a property, given discover a lender ready to offer one to. The new mortgages was registered in your residential property title or action in your order they exists and therefore there can be good pecking purchase if there is borrower standard. Once the 1 st status bank constantly gets fully settled through to the 2 nd and therefore-into the, discover deeper risks getting lenders expected to get into 2 nd or step three rd position and you will rates would-be highest during the settlement.

You can find higher risks for the private financing for both the debtor while the bank. As such, the interest costs and will set you back might be more high. A debtor needs to examine the total price of financing against the pros he/she usually get to.

The way the Financial Tends to make their funds

Credit cash is like any businesses: score for cheap, sell for far more. It should started because the no surprise one lenders want to earn a profit out of your financing. Conventional lender loan providers make their here earnings over the years, possibly a twenty five-seasons financial relationship, and they profit toward that provides other banking characteristics and you will charge. The production of money is inspired by coupons/chequing deposits and organization dealers, such as for example your retirement finance. The essential difference between the interest rate the lender costs you and the price of cash is known as give. In the bequeath, the lender will pay their costs and you may produces its money. A regular financial give is step 1.8% annually, and you can a great deal continues on for many years.

Deja una respuesta